CIC Research: Comparison and Thinking of Chinese and American Data Center Industry

Text / Sina financial opinion leader (WeChat public number kopleader) column agency CIC research

In stark contrast to the recent mergers and acquisitions in the US data center market, Chinese companies are also lacking in investment M&A in the US data center industry, with few successful cases.

CIC Research: Comparison and Thinking of Chinese and American Data Center Industry

CIC Research: Comparison and Thinking of Chinese and American Data Center Industry

In recent years, with the rapid development of cutting-edge technology fields such as big data, cloud computing, and artificial intelligence (AI), data applications have received more and more attention from people. The interpretation of human social activities and behavioral habits from the back of data has formed for the new economic model. Lay the foundation. The data has been degenerated into an asset from the previous technical tools of calculation, statistics and measurement, and its investment value has been increasingly recognized by the market, and related industries have become a new growth point in the economic development of various countries. As the upstream of the industry chain, the data center has been re-recognized.

The data center has the attributes of different industries: from a technical point of view, it is first an extension of the IT system, from the server physical unit of the hardware to the operating system of the software. The core assets held by the data center are electronic computer technology and network communication. A key component of technology. From the perspective of income model, since data center construction needs to hold or lease a large area of ​​real estate industry, the appreciation of land and buildings and rental returns are one of the important sources of income for data centers. The construction and operation of the data center has something in common with real estate projects. From the perspective of industrial structure, the data center is closely related to the surrounding environment. Adequate power supply, low electricity prices, abundant water sources, and cold environment are all key factors affecting the data center. Therefore, the data center has infrastructure assets. Attributes.

Compared with the United States, we find that China's data center service industry is still in the stage of extensive development. The market is still dominated by the monopoly of telecom operators. The network interaction services between operators are lacking, especially the data center. The market for third-party data services with economies of scale needs to be strengthened.

In stark contrast to the recent mergers and acquisitions in the US data center market, Chinese companies are also lacking in investment M&A in the US data center industry, with few successful cases. The reason is that the data belongs to sensitive industries and is regulated by governments. Second, operators in the United States have occupied the backbone of the backbone network (Carrier Hotel), forming a substantial monopoly.

In view of the key role of data in future economic growth, we suggest that the data be redefined as a strategic resource at the national level; learn from the successful experience of the development of the US data service industry, and vigorously support the development of related industries through the inclination of taxation and other policies. Formulate the "data sovereignty law", regulate the data collection and management of domestic social and commercial activities, protect national data security; change the monopoly of the telecom operators, introduce a competitive mechanism, and cultivate leading enterprises in the data service industry; and encourage domestic related enterprises Going abroad, participating in the overseas data industry chain division through investment and mergers and acquisitions, and carrying out industrial layout in the world to seize the strategic commanding heights.

First, data is an asset, data center value rediscovery

Since the world's first data processing system for aircraft reservation management was launched in 1960, after the opening of the enterprise data center, the data center experienced the popularity of computer servers in the 1980s, the Internet wave in the 1990s, the rise of cloud computing and big data in the 21st century. Its infrastructure has also changed from the initial "technology-led" to "business demand-led", and gradually established the development path of "low cost, easy maintenance, easy expansion, intelligent, on-demand service", and more and more close to the terminal. The daily life of the user.

The continuous upgrading of technology has led to a significant increase in the processing power of data centers. More and more companies need to rely on the powerful processing power of the data center to improve business efficiency. However, the construction of the data center itself faced huge cost expenses, which led to the emergence of the "data center service" industry. Data center service refers to the business model in which data center operators open their own data center resources to external users through leasing, hosting, etc., and charge a certain fee.

The initial data center services are mostly provided by basic telecom operators, mainly providing basic hosting services such as site, power and bandwidth. Later, with the expansion of the industry scale, a special third-party data center service provider company emerged, and the service scope was expanded to high value-added fields such as data management, security protection, application hosting, and on-demand customization.

According to IDC statistics, the scale of the global data center service industry has gradually expanded. Although the period of supply and demand imbalances such as the Internet bubble collapse and financial crisis has experienced, the overall growth trend has not changed.

Second, the comparison of Chinese and American data center industry

(1) At the development stage, the United States entered the stage of industry integration, and China is still in a rough development period based on new construction.

The US market is the largest and China has the strongest growth potential. From the perspective of data center distribution, the United States has a global data center share of 45%, followed by China and Japan, accounting for 8% and 7% respectively. From the growth rate of each region, according to the IDC circle forecast, the global average annual growth rate of global data centers in 2012-2017 is 17%, while that in China is 40%, and the growth rate is much higher than the global level. Compared with the United States, China's data center has huge room for development.

The current data center in the United States has entered the stage of industry integration, mainly focusing on reconstruction and expansion, and gradually entering the stage of achieving strong alliance through mergers and acquisitions, and the proportion of new data centers is not large. The US data center is gradually turning to reform and expansion, while the construction of China's data center is still in the rough development stage of new construction.

(2) From the perspective of competition, the United States is dominated by third-party data centers, while Chinese telecom operators dominate.

Data center services are primarily provided by basic telecommunications carriers and third-party data center service providers. In the US market, third-party data operators dominate, with greater scale and technological advantages; while telecom operators are gradually withdrawing and returning to the main telecommunications business, mainly because third-party data operators have more cost advantages. . In the Chinese market, telecom operators have the advantage of resource monopoly, and their market size accounts for about two-thirds of the entire data center service market. Third-party data center service providers have received restrictions on development.

(3) Geographical distribution, the data centers of China and the United States are concentrated in the central cities, and the decision-making of third-party data centers in China is relatively passive.

Judging from the location selection results, the construction of the data center in China and the United States has something in common: initially, around the first-tier cities in the center, and then considering the factors of power resources, climate, land and geological conditions, gradually expanded to second- and third-tier cities.

However, the development process of the US and China data centers is slightly different. The formation of data center nodes in the United States is formed by the convergence of networks of multiple operators. The data center has a relatively neutral position on the nodes and has an important middleman position in the data cross-network. China's data center nodes are mainly dominated by China Telecom and China Unicom. The data center does not have a strong intermediary role in the data cross-network link, so it is relatively passive in site selection.

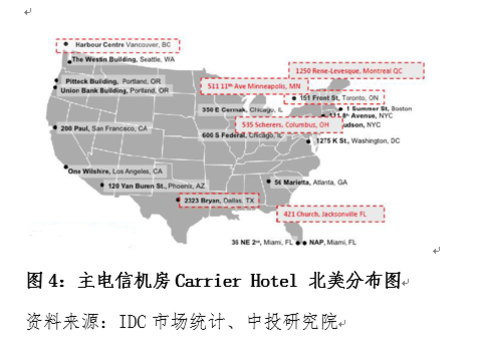

The North American data center is developed around the central city's Carrier Hotel. US data center demand is mainly concentrated in the capital (Washington area), financial center (New York, Chicago area) and technology center (San Francisco, Seattle area). These regions have also gradually formed the most important fiber backbone nodes in the United States. In the geographical pattern, a large number of fiber-optic networks meet at the backbone nodes, gradually forming a physical distribution of the Carrier Hotel, that is, a safe place or building where the fiber-optic network communication nodes are concentrated. There are about 20 main telecom engine rooms in North America, all of which are located in larger cities. Among them, mega-cities such as New York and Chicago have two main telecommunications rooms, and most of them have only one.

The North American telecommunications industry is highly market-oriented and facilitates cross-operator communication and interactive services. The North American telecommunications industry is highly market-oriented and highly competitive. In order to reduce costs and improve data exchange efficiency, communication and data transmission between operators' networks becomes an important way. The main telecom equipment room provides Meet-Me-Room (MMR) data exchange service for this purpose. MMR refers to providing direct connection between different telecom operators through cross-connect, or third-party server and telecom operation. Data connection between businesses.

Different from the US carriers' communication and communication services, the development of China's data centers is built around the backbone network structure of the backbone operators (China Telecom and China Unicom), and the cross-network information interaction services are lacking. From the perspective of Internet access bandwidth and access speed in data center rooms, Beijing, Shanghai and Guangzhou have unique network advantages. In the central and western regions, the cost of network connectivity is high, and the gap in industry service levels is huge.

Third, China's investment in mergers and acquisitions in the US data center related companies are weak

In stark contrast to the recent mergers and acquisitions in the US data center market, Chinese companies are extremely weak in investing in the US data center industry.

Due to economies of scale, the vast majority of transaction data centers in the US data center market are strategic buyers rather than financial investors, and are data center operators and service providers seeking to increase added value or expand their geographic footprint. Chinese-funded enterprises are difficult to get involved because of the sensitivity of data-related assets, difficulty in obtaining backbone nodes, lack of existing network layout, and possible foreign mergers and acquisitions review.

A rare case is that Shagang Group acquired the control of Global Switch, a London-based data center operator, in June 2017 for RMB 22 billion. Global Switch is a leading data center operator in Europe and Asia Pacific with 10 data centers, mainly located in seven core cities including London, Paris, Amsterdam, Madrid, Frankfurt, Singapore and Sydney.

Fourth, the US data center industry's enlightenment to China and related policy recommendations

Looking at the development of the US data center service industry, we can get the following inspirations.

Revelation 1: Market competition is the mainstream, and scale effect is the core

The US data center market is market-oriented, emphasizing careful division of labor and optimal allocation of resources. As a heavy investment industry, the data center has invested heavily in the early stage. As a result of higher industry concentration, third-party data operators are constantly seeking to expand their scale and optimize storage utilization, gradually occupying a dominant position in the industry, while traditional large-scale telecom operators are re-established. Focus on the main business and gradually withdraw from the data center business.

In addition, because the US telecommunications market is more open, third-party data carriers are less restricted by telecom operators, and cross-network communication can be realized through the Carrier Hotel and MMR Telecom-Me-Room to optimize data transmission. Path to achieve more efficient service.

An important reason for the lag in the development of China's data center industry is that there is less demand for network interaction between enterprises and lack of vitality for market competition. Many well-funded companies, especially large state-owned enterprises, are in the interest of data security and tend to hold data centers instead of third-party services. However, with the development of network technology, the construction of public data centers is usually more professional and the security protection is more strict. The data is not the same as the physical assets such as gold. “It’s safer to put it in your own warehouse.†This concept is too one-sided. To change this situation, the most important thing is to introduce market competition mechanism, improve the competitiveness of China's data center enterprises, and revitalize the entire industry chain.

Throughout the US and European markets, most data center operators have formed large-scale industry giants through mergers and acquisitions, using scale effects to reduce costs and improve competitiveness. In China's data center industry, market-oriented leading enterprises like this have not yet formed. China's data center service industry should also introduce appropriate market competition mechanisms to cultivate leading enterprises.

Revelation 2: Promoting Big Data Strategy at the National Level

The Obama administration launched the "Big Data Research and Development Program" in March 2012. This is another major technology deployment in the United States following the announcement of the "Information Highway" in 1993. It is proposed to be in scientific research, environmental protection, and biomedical research. Breakthroughs in the use of big data technologies in areas such as education and national security. The program involves six federal government departments, including the National Science Foundation, the US Department of Energy, and the US Department of Defense. More than 200 million research grants are spent on the development of related tools and technologies.

The "White Data White Paper 2014" released by the White House mentioned: "The outbreak of big data brings greater power to the government and creates enormous resources for the society. If the correct development strategy is implemented during this period, it will give With the driving force of the United States, the United States will continue to maintain its long-standing international competitiveness."

The big data development strategy has formed a mobilization pattern in the United States, reflecting the United States' consistent pursuit of strategies and practices in terms of innovation capabilities, industrial capabilities, information capabilities, and social management capabilities. The data is hailed as the "oil" in the information age of the 21st century. Through the development of the big data strategy in the United States, we can see that a major change is taking place globally, and the prosperity of the data center industry has officially benefited from this background. .

We suggest that the government should carry out a series of policy revisions and related legislation to promote the healthy and orderly development of the data service industry. The specific recommendations are:

(1) Promote data to strategic resources at the national level. Data is more than just an asset. Today, with the rapid development of information technology, it should be seen as a strategic resource at the national level. The hidden commercial interests behind the collection, storage, management and reuse of data will have a serious impact on the country's social stability and commercial security. In the future world competition, data is the basic support, and the key data is obtained, which is the first opportunity in the competition.

Big data is widely used in many important fields, such as earth information science, finance, information technology, and national defense. The development of big data technology will be a common task in many industries and fields in China. However, at present, the understanding of big data in all walks of life in China is not mature enough. It requires the cooperation of the government, academic circles and industry to promote consensus on this issue.

(2) Formulating a data sovereignty law. Data sovereignty is the core performance of national sovereignty in cyberspace. Data power can be divided into data management rights and data control rights. The former is the management right of the transmission, transmission and generation, processing, dissemination, utilization, transaction, storage, etc. of the domestic data, and the jurisdiction over disputes in the data field. The latter refers to the sovereign state's protection of national data to protect its data from the dangers of being monitored, falsified, forged, damaged, stolen, leaked, etc. The goal is to ensure the security, authenticity and integrity of the data. Confidentiality.

The sovereign security of national data is different from the traditional security pointed out by traditional territorial, territorial, and airspace sovereignty. Data sovereignty points to non-traditional security. The special feature is that there is no physical space boundary, and many fields involved in the digital society are all the same. Data support and expression are needed, and security in these areas has been taken into account by the overall national security concept. Therefore, it is necessary to construct a system of rules and regulations that can protect the overall national security from the height of sovereignty, that is, to build the “national data sovereignty under the overall national security conceptâ€, whose main function is to maintain the overall national security in the new risk society.

Governing data according to law is a common practice in Europe and the United States. In contrast, the construction of data-sovereign-related laws in China is obviously lagging behind developed countries in Europe and the United States. Improving the construction of relevant legal systems as soon as possible is the key to ensuring information security in China.

(3) Supporting the development of data centers through taxation and other policies. According to the Associated Press report, at least 23 states in the United States have tax incentives for data centers. In addition, 16 states have provided data center projects that encourage the use of general economic development programs. In the past 10 years, the United States has provided tax benefits for data centers worth about $1.5 billion.

The tax incentives directly stimulated the rapid development of the US data center service industry. In addition to studying the US experience and establishing relevant tax policies, combined with China's national conditions, we can also consider introducing appropriate data-based guidance measures to introduce data center industries into economically backward areas and combine them with national poverty alleviation policies. For example, the construction of data centers in Guizhou Province has greatly improved the local income level and activated the regional economy while protecting the local natural ecology. Such experience can be promoted in the western provinces of the vast majority of the centers through state support.

On the other hand, despite the broad prospects of the industry, from the development experience of the US data center, it is not possible to relax the vigilance against the risk of short-term oversupply in the industry. The development of data centers needs to be combined with local actual needs, and we must not blindly follow the trend and avoid a swarm of buzz development.

Revelation 3: The strong mobile digital consumption in the United States is the fundamental driving force for growth

The rapid growth of mobile devices such as mobile phones and cloud computing has caused the explosive growth of data traffic to be the main driving force for the expansion of market demand. According to Cisco's forecast, by 2021, mobile data traffic will account for 20% of total data traffic, in 2016 this figure will be 8%; mobile network connection speed will increase by 3 times; machine-to-machine (M2M) connection will account for mobile 29% of the total number of connections (3.3 billion), compared with 5% (7.8 billion) in 2016, the total number of smartphones will account for more than 50% (6.2 billion) of the total global equipment and connections, compared to 2016 The 3.6 billion has grown substantially. Affected by this, US consulting agencies expect to double the size of the North American data center industry by 2021.

Compared with the United States, China's mobile market still has great potential. We propose to increase supply-side reforms, deepen the mobile market in the central and western regions, and lay the foundation for the overall layout planning of China's data center service industry.

From the experience of the United States, we can see that the data traffic generated by cloud computing and ordinary consumers on mobile terminals such as mobile phones is the main reason for the growth of the data center industry. Although the growth rate of mobile communication in China is in the top position in the world, the distribution is very uneven. In the remote western provinces and autonomous regions, mobile communication is usually only used for telephone communication, and the high value-added digital consumption and mobile application market is still in the early stage of development. China's vast hinterland and a market with a large consumer population provide unlimited potential for the development of the data industry. Especially in the Midwest, the temperature is low and the water resources are abundant, which is very suitable for the construction of large data centers.

Revelation 4: M&A activity in the US and global data center services market is active

Mergers and acquisitions have had a significant impact on the data center industry in 2016 and will continue in 2017. The demand for cloud services is global, and industry leaders with global presence in the future will be more competitive. Through mergers and acquisitions, data center operators can not only effectively reduce competition, but also quickly penetrate key areas. More importantly, the increase in economies of scale can significantly reduce operating costs.

Representative M&A activities in 2016 included: Equinix acquired Verizon's data center portfolio in December 2016, which will include 29 data centers in the US and Latin America; Medina Capital and BC Partners in 2016 Fourth Century acquires CenturyLink data center business; Digital Bridge acquires DataBank's six data centers in Dallas, Minneapolis, Kansas City; TierPoint acquired CoSentry in its first quarter of 2016 for its growing portfolio Added nine data centers in the Midwestern United States.

Due to the central role of data in future economic development, we recommend that the state encourage support for Chinese companies to conduct overseas data-related asset acquisitions. Although each country regards data as a sensitive resource, it may encounter government or other conflicts in the early stage of overseas mergers and acquisitions by Chinese companies. However, through the cooperation with the relevant companies in the United States, entering as a financial investor is a worthwhile way to try. In particular, Chinese investment companies, as the country's sovereign wealth funds, should play the role of the "geese geese" model.

Disclaimer:

The information contained in this report has been obtained or authorized by lawful channels in accordance with industry-wide guidelines. The relevant content is compiled by the China Investment Research Institute according to the original text, and represents only the original author's personal or institutional views, and has nothing to do with CIC and China Investment Research Institute. The research originality and citation content have not been confirmed by CIC and China Investment Research Institute, and no guarantee or commitment is made to CIC and CIC Research Institute for the authenticity, completeness and timeliness of all or part of the content and text. The reader is only for reference, and please verify the content yourself.

About China Investment Research Institute:

CIC Research Institute is based on providing effective research support and relatively independent reference for CIC's strategic and internal investment decisions. On this basis, it will build policy recommendations for the country to provide financial and economic reforms. The long-term goal is to build A “think tank†for social and international influences and a “talent pool†for stocking and nurturing talent for the company and the Chinese financial system.

(Handwriting: Liu Shaowei, Zhang Wei, Xiao Xia, Lu Yuling, Fang Bo)

(The author of this article: CIC Research Institute is based on providing independent, objective and forward-looking research support for CIC's strategic and internal investment decisions.)

Linen Viscose Big Slub Print,Linen Viscose Print,Cotton Spandex Print Twill,Big Stripe Print With Flower

Shaoxing Sinofashion Textiles Co.,Ltd. , https://www.shownaturetex.com